Compound Interest: Comprehensive Notes

Welcome to our detailed guide on Compound Interest. Whether you're a student exploring financial mathematics or someone looking to enhance your understanding of investment growth, this guide offers thorough explanations, properties, and a wide range of examples to help you master the fundamentals of compound interest.

Introduction

Compound Interest is a fundamental concept in finance and mathematics, representing the interest calculated on the initial principal and also on the accumulated interest from previous periods. Unlike simple interest, which is calculated only on the principal amount, compound interest can significantly increase the growth of investments or the cost of loans over time. Understanding compound interest is essential for making informed financial decisions, such as investments, savings, loans, and mortgages.

Basic Concepts of Compound Interest

Before delving into calculations, it's important to grasp the foundational concepts that make compound interest operations possible.

What is Compound Interest?

Compound Interest is the interest calculated on both the initial principal and the accumulated interest from previous periods. This means that interest is earned on interest, leading to exponential growth over time.

Key Terms

- Principal (P): The initial amount of money invested or borrowed.

- Rate of Interest (r): The annual percentage rate at which interest is charged or earned.

- Time (t): The period for which the money is invested or borrowed, typically in years.

- Compounding Frequency (n): The number of times interest is compounded per year (e.g., annually, semi-annually, quarterly, monthly).

- Amount (A): The total value after interest has been applied.

- Compound Interest (CI): The interest earned on both the principal and the accumulated interest.

Properties of Compound Interest

Understanding the properties of compound interest is crucial for performing accurate calculations and interpreting results correctly.

Exponential Growth

Compound interest leads to exponential growth of the investment or debt, as interest is calculated on an increasingly larger principal amount.

Example: Investing $1,000 at 5% interest compounded annually will grow faster than the same amount at simple interest.

Compounding Frequency Impact

The frequency with which interest is compounded significantly affects the total amount of interest earned or owed. The more frequently interest is compounded, the greater the amount of compound interest.

Example: Interest compounded monthly will yield more than interest compounded annually at the same rate.

Time Factor

The time period over which interest is compounded plays a crucial role in the growth of the investment or debt. Longer periods result in more compound interest.

Example: Investing for 10 years will accumulate more interest than investing for 5 years at the same rate and compounding frequency.

Calculations with Compound Interest

Working with compound interest involves various types of calculations, including finding the future amount, the compound interest earned, the principal, the rate, the time, and the compounding frequency.

Formula for Compound Interest

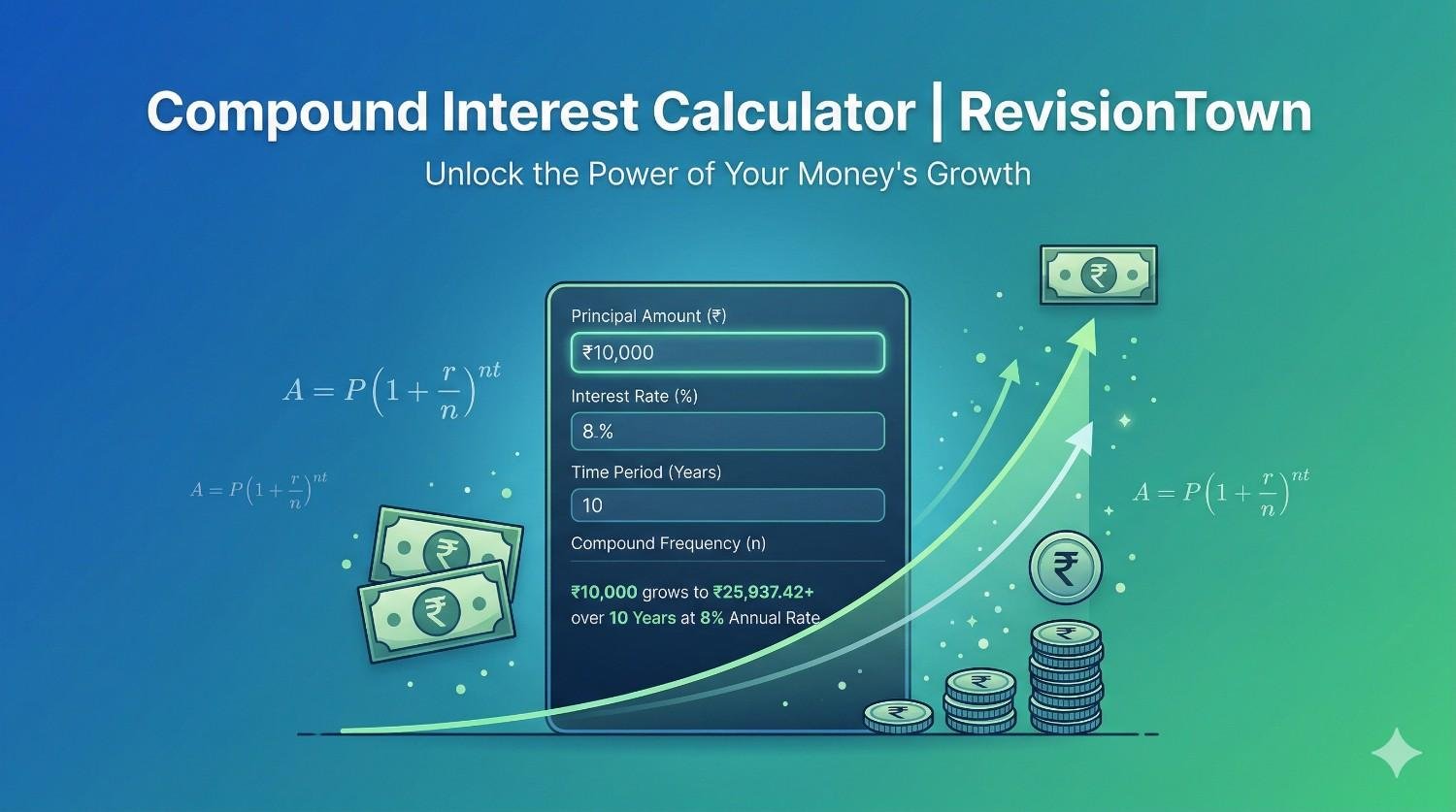

The fundamental formula to calculate the future amount with compound interest is:

A = P × (1 + r/n)^(n×t)

Where:

- A: The future amount of money after interest.

- P: The principal investment amount (initial deposit or loan amount).

- r: The annual interest rate (decimal).

- n: The number of times that interest is compounded per year.

- t: The time the money is invested or borrowed for, in years.

Example: Calculate the amount on a $1,000 investment at an annual interest rate of 5%, compounded annually for 3 years.

A = 1000 × (1 + 0.05/1)^(1×3) = 1000 × (1.05)^3 ≈ 1000 × 1.157625 = $1,157.63

Finding the Compound Interest

To calculate the compound interest earned or owed:

Formula: CI = A - P

Example: Using the previous example, the compound interest is:

CI = 1157.63 - 1000 = $157.63

Finding the Principal

To determine the original principal amount when the future amount, rate, time, and compounding frequency are known:

Formula: P = A / (1 + r/n)^(n×t)

Example: If the future amount is $1,500 after 5 years at an annual interest rate of 6%, compounded semi-annually, the principal is:

P = 1500 / (1 + 0.06/2)^(2×5) = 1500 / (1.03)^10 ≈ 1500 / 1.343916 ≈ $1,117.16

Finding the Rate of Interest

To calculate the annual interest rate when the future amount, principal, time, and compounding frequency are known:

Formula: r = n × [(A/P)^(1/(n×t)) - 1]

Example: If $2,000 grows to $2,500 in 4 years, compounded quarterly, the rate is:

r = 4 × [(2500/2000)^(1/(4×4)) - 1] ≈ 4 × [1.25^(1/16) - 1] ≈ 4 × [1.0147 - 1] ≈ 4 × 0.0147 ≈ 0.0588 or 5.88%

Finding the Time Period

To determine the time period required for an investment to reach a certain amount with compound interest:

Formula: t = [ln(A/P)] / [n × ln(1 + r/n)]

Example: How long will it take for $1,500 to grow to $2,000 at an annual interest rate of 4%, compounded monthly?

t = [ln(2000/1500)] / [12 × ln(1 + 0.04/12)] ≈ [ln(1.3333)] / [12 × ln(1.003333)] ≈ 0.2877 / (12 × 0.003327) ≈ 0.2877 / 0.03992 ≈ 7.21 years

Examples of Compound Interest

Understanding through examples is key to mastering compound interest. Below are a variety of problems ranging from easy to hard, each with detailed solutions.

Example 1: Basic Compound Interest Calculation

Problem: Calculate the amount on a principal of $1,000 at an annual interest rate of 5% compounded annually for 3 years.

Solution:

A = 1000 × (1 + 0.05/1)^(1×3) = 1000 × (1.05)^3 ≈ 1000 × 1.157625 = $1,157.63

CI = 1157.63 - 1000 = $157.63

Therefore, the amount after 3 years is $1,157.63, and the compound interest earned is $157.63.

Example 2: Compound Interest with Multiple Compounding Periods

Problem: A deposit of $2,500 is made at an annual interest rate of 4%, compounded quarterly. Calculate the amount after 5 years.

Solution:

A = 2500 × (1 + 0.04/4)^(4×5) = 2500 × (1.01)^20 ≈ 2500 × 1.22019 ≈ $3,050.48

CI = 3050.48 - 2500 = $550.48

Therefore, the amount after 5 years is approximately $3,050.48, and the compound interest earned is $550.48.

Example 3: Determining the Principal

Problem: If the amount after 6 years is $3,000 at an annual interest rate of 5%, compounded semi-annually, what was the principal?

Solution:

P = 3000 / (1 + 0.05/2)^(2×6) = 3000 / (1.025)^12 ≈ 3000 / 1.34489 ≈ $2,231.92

Therefore, the principal was approximately $2,231.92.

Example 4: Calculating the Rate of Interest

Problem: A principal of $1,800 grows to $2,500 in 4 years, compounded annually. What is the annual interest rate?

Solution:

A = 1800 × (1 + r)^4 = 2500

(1 + r)^4 = 2500 / 1800 ≈ 1.3889

1 + r = (1.3889)^(1/4) ≈ 1.0834

r ≈ 0.0834 or 8.34%

Therefore, the annual interest rate is approximately 8.34%.

Example 5: Finding the Time Period

Problem: How long will it take for an investment of $2,000 to grow to $3,000 at an annual interest rate of 6%, compounded monthly?

Solution:

A = 2000 × (1 + 0.06/12)^(12×t) = 3000

(1.005)^(12t) = 1.5

ln(1.5) = 12t × ln(1.005)

t = ln(1.5) / (12 × ln(1.005)) ≈ 0.4055 / (12 × 0.004988) ≈ 0.4055 / 0.05986 ≈ 6.78 years

Therefore, it will take approximately 6.78 years for the investment to grow to $3,000.

Word Problems: Application of Compound Interest

Applying compound interest to real-life scenarios enhances understanding and demonstrates its practical utility. Here are several word problems that incorporate these concepts, along with their solutions.

Example 1: Investment Growth

Problem: John invests $5,000 in a bond that offers an annual compound interest rate of 7%, compounded annually. How much will his investment be worth after 10 years?

Solution:

A = 5000 × (1 + 0.07)^10 ≈ 5000 × 1.967151 ≈ $9,835.76

CI = 9835.76 - 5000 = $4,835.76

Therefore, John's investment will be worth approximately $9,835.76 after 10 years, with a compound interest earned of $4,835.76.

Example 2: Loan Repayment

Problem: Sarah takes out a loan of $3,000 at an annual interest rate of 5%, compounded monthly. She plans to repay the loan in 4 years. What is the total amount she will have to repay?

Solution:

A = 3000 × (1 + 0.05/12)^(12×4) ≈ 3000 × (1.0041667)^48 ≈ 3000 × 1.221392 ≈ $3,664.18

CI = 3664.18 - 3000 = $664.18

Therefore, Sarah will have to repay a total of $3,664.18, with a compound interest of $664.18.

Example 3: Savings Account Growth with Additional Deposits

Problem: Emma deposits $1,200 into a savings account that offers an annual compound interest rate of 4%, compounded quarterly. After 3 years, she deposits an additional $800 into the same account. Calculate the total amount in her account after 5 years.

Solution:

First Deposit:

A1 = 1200 × (1 + 0.04/4)^(4×3) = 1200 × (1.01)^12 ≈ 1200 × 1.126825 ≈ $1,352.19

Second Deposit:

A2 = 800 × (1 + 0.04/4)^(4×2) = 800 × (1.01)^8 ≈ 800 × 1.082856 ≈ $866.29

Total Amount = A1 + A2 ≈ 1352.19 + 866.29 ≈ $2,218.48

Therefore, the total amount in Emma's account after 5 years is approximately $2,218.48.

Example 4: Retirement Fund Growth

Problem: Noah invests $10,000 in a retirement fund that earns an annual compound interest rate of 6%, compounded monthly. How much will his investment be worth after 20 years?

Solution:

A = 10000 × (1 + 0.06/12)^(12×20) ≈ 10000 × (1.005)^240 ≈ 10000 × 3.310204 ≈ $33,102.04

CI = 33102.04 - 10000 = $23,102.04

Therefore, Noah's investment will be worth approximately $33,102.04 after 20 years, with a compound interest of $23,102.04.

Example 5: Education Savings Plan

Problem: Ava wants to save $8,000 for her college education. She decides to invest $5,000 now in a fund that offers an annual compound interest rate of 5%, compounded semi-annually. How much more does she need to invest now to reach her goal in 4 years?

Solution:

Future Value Needed: $8,000

First Investment:

A1 = 5000 × (1 + 0.05/2)^(2×4) = 5000 × (1.025)^8 ≈ 5000 × 1.218402 ≈ $6,092.01

Amount Still Needed: 8000 - 6092.01 ≈ $1,907.99

To find the additional principal (P2) required to earn $1,907.99 in 4 years at 5% compounded semi-annually:

A2 = P2 × (1 + 0.05/2)^(2×4) = P2 × (1.025)^8 ≈ P2 × 1.218402

P2 = 1907.99 / 1.218402 ≈ $1,564.00

Therefore, Ava needs to invest an additional $1,564 now.

Therefore, Ava needs to invest an additional approximately $1,564 now to reach her goal of $8,000 in 4 years.

Strategies and Tips for Working with Compound Interest

Enhancing your skills in calculating compound interest involves employing effective strategies and consistent practice. Here are some tips to help you improve:

1. Master the Fundamental Compound Interest Formula

Understand and memorize the core formula for calculating compound interest:

- Formula: A = P × (1 + r/n)^(n×t)

Example: To find the future amount on $1,000 at 5% interest compounded annually for 3 years:

A = 1000 × (1 + 0.05/1)^(1×3) = 1000 × 1.157625 = $1,157.63

2. Convert Percentages to Decimals

Always convert the interest rate from a percentage to a decimal by dividing by 100 before performing calculations.

Example: 6% = 0.06

3. Identify the Compounding Frequency

Determine how often interest is compounded (annually, semi-annually, quarterly, monthly, etc.) to apply the correct value of n in the formula.

Example: If interest is compounded quarterly, n = 4.

4. Use Logarithms for Solving Time or Rate

When solving for time or rate in compound interest problems, logarithms can be an essential tool.

Example: To solve for time in A = P × (1 + r/n)^(n×t), take the natural logarithm of both sides.

5. Practice Converting Between Forms

Regularly practice converting between percentages, decimals, and fractions to build fluency and speed in calculations.

Example: Convert 0.75 to a percentage and a fraction.

0.75 = 75%

0.75 = 3/4

6. Break Down Complex Problems

For complex compound interest problems, break them down into smaller, more manageable steps to simplify the process.

Example: To calculate compound interest with additional deposits, first calculate the future value of each deposit separately and then sum them.

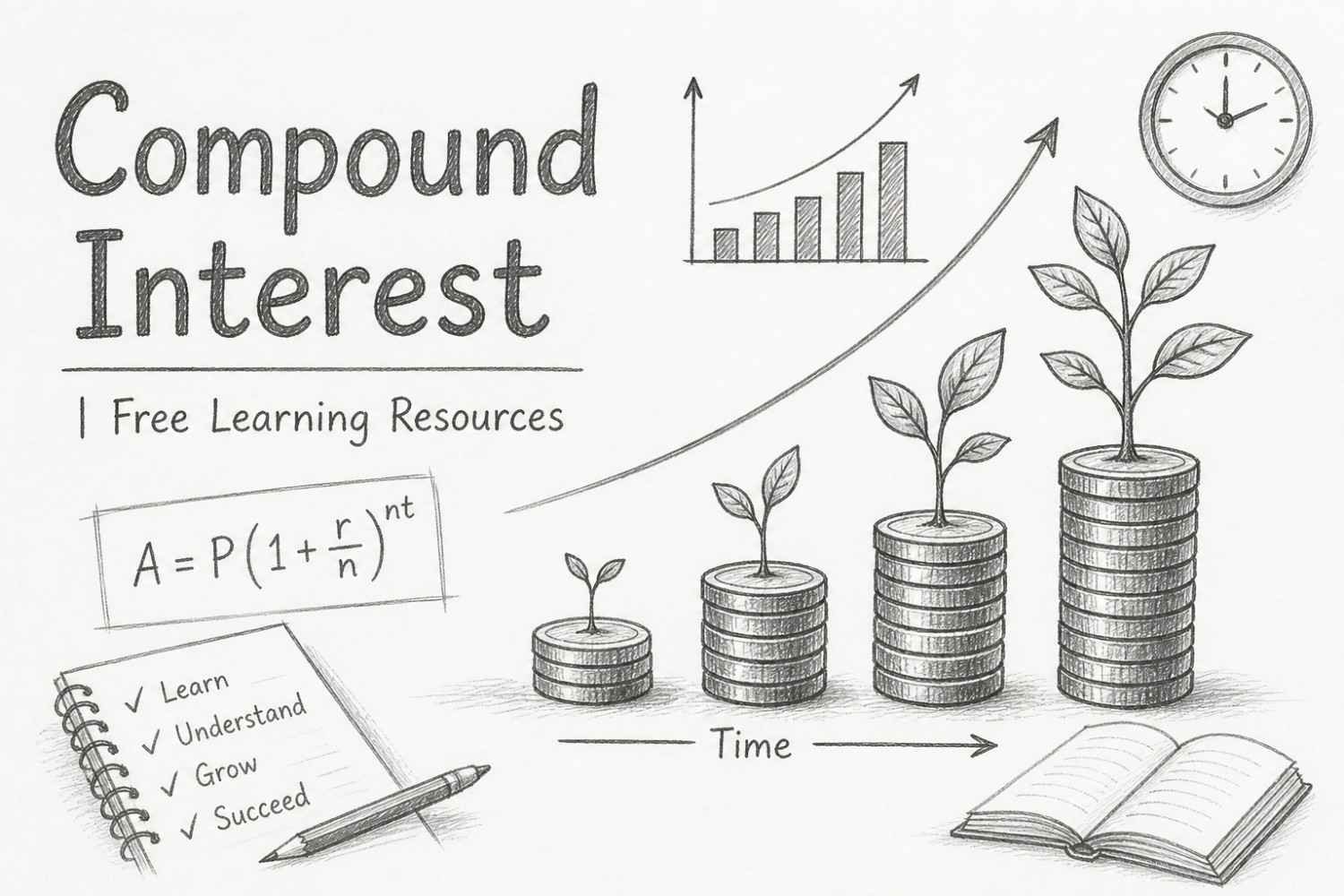

7. Use Visual Aids

Employ visual tools like charts, graphs, and diagrams to better understand and visualize compound interest relationships.

Example: A graph showing the growth of an investment over time can illustrate the effects of different interest rates and compounding frequencies.

8. Double-Check Your Work

Always review your calculations to catch and correct any mistakes. Verify by plugging the found value back into the original formula.

Example: After calculating the future amount, use the formula again to ensure it matches the expected value.

9. Apply Real-Life Scenarios

Use real-life situations to practice compound interest calculations, making the concepts more relatable and easier to understand.

Example: Calculate the future value of your savings account or the total amount owed on a loan with compound interest.

10. Teach Others

Explaining compound interest concepts to someone else can reinforce your understanding and highlight any areas needing improvement.

Example: Help a friend calculate the future value of their investments or loans.

Common Mistakes in Compound Interest and How to Avoid Them

Being aware of common errors can help you avoid them and improve your calculation accuracy.

1. Confusing Compound Interest with Simple Interest

Mistake: Using the simple interest formula instead of the compound interest formula.

Solution: Ensure you are using the correct formula based on whether interest is compounded or not.

Example:

Incorrect: SI = P × R × T / 100

Correct: A = P × (1 + r/n)^(n×t)

2. Forgetting to Convert Percentages to Decimals

Mistake: Performing calculations without converting the interest rate from a percentage to a decimal.

Solution: Always divide the interest rate by 100 to convert it to a decimal before using it in the formula.

Example:

Incorrect: A = 1000 × (1 + 5/100)^3 = 1000 × 1.05^3 = 1157.63

Correct: A = 1000 × (1 + 0.05)^3 = 1000 × 1.157625 = $1,157.63

3. Using the Wrong Compounding Frequency

Mistake: Incorrectly identifying the number of compounding periods per year, leading to wrong calculations.

Solution: Carefully determine how often interest is compounded (e.g., annually, semi-annually, quarterly, monthly) and use the correct value of n in the formula.

Example:

Incorrect: Compounded annually, n = 12

Correct: Compounded monthly, n = 12

4. Misapplying the Compound Interest Formula

Mistake: Incorrectly setting up or rearranging the compound interest formula when solving for different variables.

Solution: Familiarize yourself with the formula and practice rearranging it to solve for different variables like P, r, t, or A.

Example:

To solve for P: P = A / (1 + r/n)^(n×t)

5. Miscalculating Exponents

Mistake: Incorrectly calculating the exponent part of the formula, especially for large values of n and t.

Solution: Use a calculator to accurately compute exponents and ensure precision in your calculations.

Example:

Incorrect: (1 + 0.05/1)^3 = 1.05^3 = 1.1576

Correct: Use calculator for precise computation.

6. Overlooking Additional Deposits or Withdrawals

Mistake: Ignoring additional deposits or withdrawals when calculating compound interest, leading to inaccurate results.

Solution: Account for each deposit or withdrawal separately by calculating their future values and summing them up.

Example:

If an additional deposit is made, calculate its future value separately.

7. Rounding Off Prematurely

Mistake: Rounding off intermediate steps before completing all calculations, leading to inaccurate final results.

Solution: Keep all decimal places throughout the calculation and round off only the final answer as required.

Example:

Incorrect: A = 1000 × 1.05^3 ≈ 1000 × 1.16 = $1,160

Correct: A = 1000 × 1.157625 = $1,157.63

8. Ignoring the Time Period Alignment

Mistake: Not aligning the time period with the compounding frequency, such as using years when the compounding is monthly.

Solution: Ensure that the time period and compounding frequency are in compatible units (e.g., years with annual compounding, months with monthly compounding).

Example:

If compounding is monthly, convert years to months if necessary.

9. Misinterpreting "Of" in Compound Interest Problems

Mistake: Misunderstanding what "of" signifies in compound interest problems, leading to incorrect calculations.

Solution: Recognize that "of" indicates multiplication in compound interest problems.

Example:

Incorrect: A = P + r = P + 0.05 = 1.05P

Correct: A = P × (1 + r)^t

10. Overcomplicating Simple Problems

Mistake: Adding unnecessary steps or complexity to straightforward compound interest problems.

Solution: Simplify your approach and follow the fundamental steps for each operation using the compound interest formula directly.

Example:

Incorrect: Breaking down the formula into unrelated steps.

Correct: Use A = P × (1 + r/n)^(n×t) directly.

Practice Questions: Test Your Compound Interest Skills

Practicing with a variety of problems is key to mastering compound interest. Below are practice questions categorized by difficulty level, along with their solutions.

Level 1: Easy

- Calculate the amount on a principal of $1,000 at an annual interest rate of 5% compounded annually for 2 years.

- Find the future value after 3 years if the principal is $500 and the compound interest rate is 4%, compounded annually.

- Determine the amount on $800 invested at 6% annual interest compounded annually for 1 year.

- A loan of $300 is taken at an annual compound interest rate of 3% for 4 years. What is the amount owed?

- What is the future value to be repaid if $200 is invested at 5% compound interest annually for 2 years?

Solutions:

-

Solution:

A = 1000 × (1 + 0.05)^2 = 1000 × 1.1025 = $1,102.50 -

Solution:

A = 500 × (1 + 0.04)^3 ≈ 500 × 1.124864 ≈ $562.43 -

Solution:

A = 800 × (1 + 0.06)^1 = 800 × 1.06 = $848.00 -

Solution:

A = 300 × (1 + 0.03)^4 ≈ 300 × 1.12550881 ≈ $337.65 -

Solution:

A = 200 × (1 + 0.05)^2 = 200 × 1.1025 = $220.50

Level 2: Medium

- A principal of $2,000 earns compound interest at an annual rate of 5% for 3 years, compounded annually. What is the future value?

- Find the principal amount if the future value is $2,500 after 4 years at an annual compound interest rate of 6%, compounded semi-annually.

- Calculate the time required for $1,500 to grow to $2,000 at an annual compound interest rate of 4%, compounded quarterly.

- What is the compound interest earned on $3,000 at an annual rate of 7%, compounded annually for 5 years?

- Determine the future value of an investment of $1,200 at an annual compound interest rate of 3%, compounded monthly for 2 years.

Solutions:

-

Solution:

A = 2000 × (1 + 0.05)^3 = 2000 × 1.157625 ≈ $2,315.25

CI = 2315.25 - 2000 = $315.25 -

Solution:

P = 2500 / (1 + 0.06/2)^(2×4) = 2500 / (1.03)^8 ≈ 2500 / 1.26677 ≈ $1,973.88 -

Solution:

A = P × (1 + r/n)^(n×t)

2000 = 1500 × (1 + 0.04/4)^(4×t)

2000/1500 = (1.01)^(4t)

1.3333 ≈ (1.01)^(4t)

ln(1.3333) = 4t × ln(1.01)

0.287682 = 4t × 0.00995033

4t = 0.287682 / 0.00995033 ≈ 28.89

t ≈ 7.22 years -

Solution:

CI = A - P

A = 3000 × (1 + 0.07)^5 ≈ 3000 × 1.402551 ≈ $4,207.65

CI = 4207.65 - 3000 ≈ $1,207.65 -

Solution:

A = 1200 × (1 + 0.03/12)^(12×2) = 1200 × (1.0025)^24 ≈ 1200 × 1.061363 ≈ $1,273.64

CI = 1273.64 - 1200 ≈ $73.64

Level 3: Hard

- Determine the principal if the future value is $5,000 after 10 years at an annual compound interest rate of 5%, compounded quarterly.

- A loan of $4,500 is taken at an annual compound interest rate of 8%, compounded monthly. What is the amount owed after 6 years?

- Find the time required for an investment of $2,500 to grow to $4,000 at an annual compound interest rate of 6%, compounded semi-annually.

- What is the annual compound interest rate if a principal of $3,200 grows to $4,800 in 5 years, compounded annually?

- Calculate the compound interest earned on $10,000 at an annual rate of 4.5%, compounded monthly for 8 years.

Solutions:

-

Solution:

A = P × (1 + 0.05/4)^(4×10) = 5000

P = 5000 / (1.0125)^40 ≈ 5000 / 2.20804 ≈ $2,264.37 -

Solution:

A = 4500 × (1 + 0.08/12)^(12×6) = 4500 × (1.0066667)^72 ≈ 4500 × 1.747422 ≈ $7,863.40

CI = 7863.40 - 4500 ≈ $3,363.40 -

Solution:

A = 4000, P = 2500, r = 0.06, n = 2

4000 = 2500 × (1 + 0.06/2)^(2×t)

1.6 = (1.03)^(2t)

ln(1.6) = 2t × ln(1.03)

0.4700036 = 2t × 0.0295588

2t = 0.4700036 / 0.0295588 ≈ 15.888

t ≈ 7.94 years -

Solution:

A = 4800, P = 3200, t = 5, n = 1

4800 = 3200 × (1 + r)^5

1.5 = (1 + r)^5

1 + r = (1.5)^(1/5) ≈ 1.08447

r ≈ 0.08447 or 8.45% -

Solution:

A = 10000 × (1 + 0.045/12)^(12×8) ≈ 10000 × (1.00375)^96 ≈ 10000 × 1.432364 ≈ $14,323.64

CI = 14323.64 - 10000 ≈ $4,323.64

Practice Questions: Test Your Compound Interest Skills

Practicing with a variety of problems is key to mastering compound interest. Below are practice questions categorized by difficulty level, along with their solutions.

Level 1: Easy

- Calculate the amount on a principal of $1,200 at an annual interest rate of 5% compounded annually for 2 years.

- Find the future value after 3 years if the principal is $800 and the compound interest rate is 4%, compounded annually.

- Determine the amount on $1,000 invested at 6% annual interest compounded annually for 1 year.

- A loan of $400 is taken at an annual compound interest rate of 3% for 4 years. What is the amount owed?

- What is the future value to be repaid if $250 is invested at 5% compound interest annually for 2 years?

Solutions:

-

Solution:

A = 1200 × (1 + 0.05)^2 = 1200 × 1.1025 = $1,323.00 -

Solution:

A = 800 × (1 + 0.04)^3 ≈ 800 × 1.124864 ≈ $899.89 -

Solution:

A = 1000 × (1 + 0.06)^1 = 1000 × 1.06 = $1,060.00 -

Solution:

A = 400 × (1 + 0.03)^4 ≈ 400 × 1.125509 ≈ $450.20 -

Solution:

A = 250 × (1 + 0.05)^2 = 250 × 1.1025 = $275.63

Level 2: Medium

- A principal of $2,500 earns compound interest at an annual rate of 5% for 3 years, compounded annually. What is the future value?

- Find the principal amount if the future value is $3,000 after 4 years at an annual compound interest rate of 6%, compounded semi-annually.

- Calculate the time required for $1,800 to grow to $2,400 at an annual compound interest rate of 4%, compounded quarterly.

- What is the compound interest earned on $4,000 at an annual rate of 7%, compounded annually for 5 years?

- Determine the future value of an investment of $1,500 at an annual compound interest rate of 3%, compounded monthly for 2 years.

Solutions:

-

Solution:

A = 2500 × (1 + 0.05)^3 = 2500 × 1.157625 ≈ $2,894.06

CI = 2894.06 - 2500 ≈ $394.06 -

Solution:

P = 3000 / (1 + 0.06/2)^(2×4) = 3000 / (1.03)^8 ≈ 3000 / 1.26677 ≈ $2,366.32 -

Solution:

A = 2400, P = 1800, r = 0.04, n = 4

2400 = 1800 × (1 + 0.04/4)^(4×t)

1.3333 = (1.01)^(4t)

ln(1.3333) = 4t × ln(1.01)

0.287682 = 4t × 0.00995033

4t = 0.287682 / 0.00995033 ≈ 28.89

t ≈ 7.22 years -

Solution:

CI = A - P

A = 4000 × (1 + 0.07)^5 ≈ 4000 × 1.402552 ≈ $5,610.21

CI = 5610.21 - 4000 ≈ $1,610.21 -

Solution:

A = 1500 × (1 + 0.03/12)^(12×2) = 1500 × (1.0025)^24 ≈ 1500 × 1.061364 ≈ $1,592.05

CI = 1592.05 - 1500 ≈ $92.05

Level 3: Hard

- Determine the principal if the future value is $5,000 after 10 years at an annual compound interest rate of 5%, compounded quarterly.

- A loan of $4,500 is taken at an annual compound interest rate of 8%, compounded monthly. What is the amount owed after 6 years?

- Find the time required for an investment of $2,500 to grow to $4,000 at an annual compound interest rate of 6%, compounded semi-annually.

- What is the annual compound interest rate if a principal of $3,200 grows to $4,800 in 5 years, compounded annually?

- Calculate the compound interest earned on $10,000 at an annual rate of 4.5%, compounded monthly for 8 years.

Solutions:

-

Solution:

A = 5000, t = 10, r = 0.05, n = 4

P = 5000 / (1 + 0.05/4)^(4×10) = 5000 / (1.0125)^40 ≈ 5000 / 1.643619 ≈ $3,045.06 -

Solution:

A = 4500 × (1 + 0.08/12)^(12×6) = 4500 × (1.0066667)^72 ≈ 4500 × 1.601032 ≈ $7,204.64

CI = 7204.64 - 4500 ≈ $2,704.64 -

Solution:

A = 4000, P = 2500, r = 0.06, n = 2

4000 = 2500 × (1 + 0.06/2)^(2×t)

1.6 = (1.03)^(2t)

ln(1.6) = 2t × ln(1.03)

0.4700036 = 2t × 0.0295588

2t = 0.4700036 / 0.0295588 ≈ 15.888

t ≈ 7.94 years -

Solution:

A = 4800, P = 3200, t = 5, n = 1

4800 = 3200 × (1 + r)^5

(1 + r)^5 = 1.5

1 + r = (1.5)^(1/5) ≈ 1.08447

r ≈ 0.08447 or 8.45% -

Solution:

A = 10000 × (1 + 0.045/12)^(12×8) ≈ 10000 × (1.00375)^96 ≈ 10000 × 1.432364 ≈ $14,323.64

CI = 14323.64 - 10000 ≈ $4,323.64

Combined Exercises: Examples and Solutions

Many mathematical problems require the use of compound interest in conjunction with other operations. Below are examples that incorporate these concepts alongside logical reasoning and application to real-world scenarios.

Example 1: Investment Growth with Additional Deposits

Problem: Olivia invests $3,000 in a savings account that offers an annual compound interest rate of 5%, compounded annually. After 4 years, she invests an additional $2,000 into the same account at the same interest rate for another 3 years. Calculate the total amount in her account after 7 years.

Solution:

First Investment:

A1 = 3000 × (1 + 0.05)^4 ≈ 3000 × 1.215506 ≈ $3,646.52

Second Investment:

A2 = 2000 × (1 + 0.05)^3 ≈ 2000 × 1.157625 ≈ $2,315.25

Total Amount = A1 + A2 ≈ 3646.52 + 2315.25 ≈ $5,961.77

Therefore, the total amount in Olivia's account after 7 years is approximately $5,961.77.

Example 2: Loan Repayment with Interest

Problem: Liam takes out a loan of $4,500 at an annual compound interest rate of 6%, compounded monthly. He plans to repay the loan in 5 years. What is the total amount he will have to repay?

Solution:

A = 4500 × (1 + 0.06/12)^(12×5) ≈ 4500 × (1.005)^60 ≈ 4500 × 1.34885 ≈ $6,070.03

CI = 6070.03 - 4500 ≈ $1,570.03

Therefore, Liam will have to repay a total of $6,070.03, with a compound interest of $1,570.03.

Example 3: Education Savings Plan with Multiple Deposits

Problem: Ava wants to save $10,000 for her college education. She decides to deposit $5,000 now in a fund that offers an annual compound interest rate of 4%, compounded semi-annually. After 3 years, she deposits an additional $3,000 into the same fund at the same interest rate for another 2 years. Calculate the total amount in her account after 5 years.

Solution:

First Deposit:

A1 = 5000 × (1 + 0.04/2)^(2×3) = 5000 × (1.02)^6 ≈ 5000 × 1.126162 ≈ $5,630.81

Second Deposit:

A2 = 3000 × (1 + 0.04/2)^(2×2) = 3000 × (1.02)^4 ≈ 3000 × 1.082432 ≈ $3,247.30

Total Amount = A1 + A2 ≈ 5630.81 + 3247.30 ≈ $8,878.11

Therefore, the total amount in Ava's account after 5 years is approximately $8,878.11.

Example 4: Retirement Fund Growth with Regular Contributions

Problem: Noah invests $10,000 in a retirement fund that earns an annual compound interest rate of 5%, compounded monthly. He plans to contribute an additional $200 at the end of each month for 10 years. Calculate the total amount in his retirement fund after 10 years.

Solution:

Future Value of Initial Investment:

A1 = 10000 × (1 + 0.05/12)^(12×10) ≈ 10000 × (1.0041667)^120 ≈ 10000 × 1.647009 ≈ $16,470.09

Future Value of Monthly Contributions:

A2 = 200 × [((1 + 0.05/12)^(12×10) - 1) / (0.05/12)] ≈ 200 × [1.647009 - 1) / 0.0041667] ≈ 200 × [0.647009 / 0.0041667] ≈ 200 × 155.282 ≈ $31,056.40

Total Amount = A1 + A2 ≈ 16470.09 + 31056.40 ≈ $47,526.49

Therefore, the total amount in Noah's retirement fund after 10 years is approximately $47,526.49.

Example 5: Mortgage Calculation

Problem: Emma takes out a mortgage of $250,000 at an annual compound interest rate of 3.5%, compounded monthly. She plans to repay the mortgage in 30 years. What is the total amount she will pay over the life of the mortgage?

Solution:

A = 250000 × (1 + 0.035/12)^(12×30) ≈ 250000 × (1.0029167)^360 ≈ 250000 × 2.853287 ≈ $713,321.75

CI = 713321.75 - 250000 ≈ $463,321.75

Therefore, Emma will pay a total of $713,321.75 over the life of the mortgage, with a compound interest of $463,321.75.

Strategies and Tips for Working with Compound Interest

Enhancing your skills in calculating compound interest involves employing effective strategies and consistent practice. Here are some tips to help you improve:

1. Master the Fundamental Compound Interest Formula

Understand and memorize the core formula for calculating compound interest:

- Formula: A = P × (1 + r/n)^(n×t)

Example: To find the future amount on $2,000 at 6% interest compounded monthly for 4 years:

A = 2000 × (1 + 0.06/12)^(12×4) ≈ 2000 × (1.005)^48 ≈ 2000 × 1.270244 ≈ $2,540.49

2. Convert Percentages to Decimals

Always convert the interest rate from a percentage to a decimal by dividing by 100 before performing calculations.

Example: 7% = 0.07

3. Identify the Compounding Frequency

Determine how often interest is compounded (annually, semi-annually, quarterly, monthly, etc.) to apply the correct value of n in the formula.

Example: If interest is compounded monthly, n = 12.

4. Use Logarithms for Solving Time or Rate

When solving for time or rate in compound interest problems, logarithms can be an essential tool.

Example: To solve for time in A = P × (1 + r/n)^(n×t), take the natural logarithm of both sides.

5. Practice Converting Between Forms

Regularly practice converting between percentages, decimals, and fractions to build fluency and speed in calculations.

Example: Convert 0.85 to a percentage and a fraction.

0.85 = 85%

0.85 = 17/20

6. Break Down Complex Problems

For complex compound interest problems, break them down into smaller, more manageable steps to simplify the process.

Example: To calculate compound interest with additional deposits, first calculate the future value of each deposit separately and then sum them up.

7. Use Visual Aids

Employ visual tools like charts, graphs, and diagrams to better understand and visualize compound interest relationships.

Example: A graph showing the exponential growth of an investment over time can illustrate the impact of different interest rates and compounding frequencies.

8. Double-Check Your Work

Always review your calculations to catch and correct any mistakes. Verify by plugging the found value back into the original formula.

Example: After calculating the future amount, use the formula again to ensure it matches the expected value.

9. Apply Real-Life Scenarios

Use real-life situations to practice compound interest calculations, making the concepts more relatable and easier to understand.

Example: Calculate the future value of your savings account or the total amount owed on a loan with compound interest.

10. Teach Others

Explaining compound interest concepts to someone else can reinforce your understanding and highlight any areas needing improvement.

Example: Help a friend calculate the future value of their investments or loans.

Common Mistakes in Compound Interest and How to Avoid Them

Being aware of common errors can help you avoid them and improve your calculation accuracy.

1. Confusing Compound Interest with Simple Interest

Mistake: Using the simple interest formula instead of the compound interest formula.

Solution: Ensure you are using the correct formula based on whether interest is compounded or not.

Example:

Incorrect: SI = P × R × T / 100

Correct: A = P × (1 + r/n)^(n×t)

2. Forgetting to Convert Percentages to Decimals

Mistake: Performing calculations without converting the interest rate from a percentage to a decimal.

Solution: Always divide the interest rate by 100 to convert it to a decimal before using it in the formula.

Example:

Incorrect: A = 1000 × (1 + 5/100)^3 = 1000 × 1.05^3 = 1157.63

Correct: A = 1000 × (1 + 0.05)^3 = 1000 × 1.157625 = $1,157.63

3. Using the Wrong Compounding Frequency

Mistake: Incorrectly identifying the number of compounding periods per year, leading to wrong calculations.

Solution: Carefully determine how often interest is compounded (e.g., annually, semi-annually, quarterly, monthly) and use the correct value of n in the formula.

Example:

Incorrect: Compounded annually, n = 12

Correct: Compounded monthly, n = 12

4. Misapplying the Compound Interest Formula

Mistake: Incorrectly setting up or rearranging the compound interest formula when solving for different variables.

Solution: Familiarize yourself with the formula and practice rearranging it to solve for different variables like A, P, r, t, or n.

Example:

To solve for P: P = A / (1 + r/n)^(n×t)

5. Miscalculating Exponents

Mistake: Incorrectly calculating the exponent part of the formula, especially for large values of n and t.

Solution: Use a calculator to accurately compute exponents and ensure precision in your calculations.

Example:

Incorrect: (1 + 0.05/1)^3 = 1.05^3 = 1.1576

Correct: Use calculator for precise computation.

6. Overlooking Additional Deposits or Withdrawals

Mistake: Ignoring additional deposits or withdrawals when calculating compound interest, leading to inaccurate results.

Solution: Account for each deposit or withdrawal separately by calculating their future values and summing them up.

Example:

If an additional deposit is made, calculate its future value separately.

7. Rounding Off Prematurely

Mistake: Rounding off intermediate steps before completing all calculations, leading to inaccurate final results.

Solution: Keep all decimal places throughout the calculation and round off only the final answer as required.

Example:

Incorrect: A = 1000 × 1.05^3 ≈ 1000 × 1.16 = $1,160

Correct: A = 1000 × 1.157625 = $1,157.63

8. Ignoring the Time Period Alignment

Mistake: Not aligning the time period with the compounding frequency, such as using years when the compounding is monthly.

Solution: Ensure that the time period and the compounding frequency are in compatible units (e.g., years with annual compounding, months with monthly compounding).

Example:

If compounding is monthly, convert years to months if necessary.

9. Misinterpreting "Of" in Compound Interest Problems

Mistake: Misunderstanding what "of" signifies in compound interest problems, leading to incorrect calculations.

Solution: Recognize that "of" indicates multiplication in compound interest problems and apply the correct formula accordingly.

Example:

Incorrect: A = P + r = P + 0.05 = 1.05P

Correct: A = P × (1 + r/n)^(n×t)

10. Overcomplicating Simple Problems

Mistake: Adding unnecessary steps or complexity to straightforward compound interest problems.

Solution: Simplify your approach and follow the fundamental steps for each operation using the compound interest formula directly.

Example:

Incorrect: Breaking down the formula into unrelated steps.

Correct: Use A = P × (1 + r/n)^(n×t) directly.

Practice Questions: Test Your Compound Interest Skills

Practicing with a variety of problems is key to mastering compound interest. Below are practice questions categorized by difficulty level, along with their solutions.

Level 1: Easy

- Calculate the amount on a principal of $1,500 at an annual interest rate of 5% compounded annually for 2 years.

- Find the future value after 3 years if the principal is $900 and the compound interest rate is 4%, compounded annually.

- Determine the amount on $1,200 invested at 6% annual interest compounded annually for 1 year.

- A loan of $500 is taken at an annual compound interest rate of 3% for 4 years. What is the amount owed?

- What is the future value to be repaid if $300 is invested at 5% compound interest annually for 2 years?

Solutions:

-

Solution:

A = 1500 × (1 + 0.05)^2 = 1500 × 1.1025 = $1,653.75 -

Solution:

A = 900 × (1 + 0.04)^3 ≈ 900 × 1.124864 ≈ $1,012.38 -

Solution:

A = 1200 × (1 + 0.06)^1 = 1200 × 1.06 = $1,272.00 -

Solution:

A = 500 × (1 + 0.03)^4 ≈ 500 × 1.12550881 ≈ $562.75 -

Solution:

A = 300 × (1 + 0.05)^2 = 300 × 1.1025 = $330.75

Level 2: Medium

- A principal of $3,000 earns compound interest at an annual rate of 5% for 3 years, compounded annually. What is the future value?

- Find the principal amount if the future value is $3,500 after 4 years at an annual compound interest rate of 6%, compounded semi-annually.

- Calculate the time required for $2,000 to grow to $2,800 at an annual compound interest rate of 4%, compounded quarterly.

- What is the compound interest earned on $5,000 at an annual rate of 7%, compounded annually for 5 years?

- Determine the future value of an investment of $2,000 at an annual compound interest rate of 3%, compounded monthly for 2 years.

Solutions:

-

Solution:

A = 3000 × (1 + 0.05)^3 = 3000 × 1.157625 ≈ $3,472.88

CI = 3472.88 - 3000 ≈ $472.88 -

Solution:

P = 3500 / (1 + 0.06/2)^(2×4) = 3500 / (1.03)^8 ≈ 3500 / 1.26677 ≈ $2,761.50 -

Solution:

A = 2800, P = 2000, r = 0.04, n = 4

2800 = 2000 × (1 + 0.04/4)^(4×t)

1.4 = (1.01)^(4t)

ln(1.4) = 4t × ln(1.01)

0.336472 = 4t × 0.00995033

4t = 0.336472 / 0.00995033 ≈ 33.82

t ≈ 8.45 years -

Solution:

CI = A - P

A = 5000 × (1 + 0.07)^5 ≈ 5000 × 1.402552 ≈ $7,012.76

CI = 7012.76 - 5000 ≈ $2,012.76 -

Solution:

A = 2000 × (1 + 0.03/12)^(12×2) ≈ 2000 × (1.0025)^24 ≈ 2000 × 1.061363 ≈ $2,122.73

CI = 2122.73 - 2000 ≈ $122.73

Level 3: Hard

- Determine the principal if the future value is $5,500 after 10 years at an annual compound interest rate of 5%, compounded quarterly.

- A loan of $6,000 is taken at an annual compound interest rate of 8%, compounded monthly. What is the amount owed after 6 years?

- Find the time required for an investment of $3,500 to grow to $5,000 at an annual compound interest rate of 6%, compounded semi-annually.

- What is the annual compound interest rate if a principal of $4,000 grows to $6,400 in 5 years, compounded annually?

- Calculate the compound interest earned on $12,000 at an annual rate of 4.5%, compounded monthly for 8 years.

Solutions:

-

Solution:

A = 5500, t = 10, r = 0.05, n = 4

P = 5500 / (1 + 0.05/4)^(4×10) = 5500 / (1.0125)^40 ≈ 5500 / 1.643619 ≈ $3,348.32 -

Solution:

A = 6000 × (1 + 0.08/12)^(12×6) ≈ 6000 × (1.0066667)^72 ≈ 6000 × 1.747422 ≈ $10,484.53

CI = 10484.53 - 6000 ≈ $4,484.53 -

Solution:

A = 5000, P = 3500, r = 0.06, n = 2

5000 = 3500 × (1 + 0.06/2)^(2×t)

1.4286 = (1.03)^(2t)

ln(1.4286) = 2t × ln(1.03)

0.356675 = 2t × 0.0295588

2t = 0.356675 / 0.0295588 ≈ 12.07

t ≈ 6.04 years -

Solution:

A = 6400, P = 4000, t = 5, n = 1

6400 = 4000 × (1 + r)^5

(1 + r)^5 = 1.6

1 + r = (1.6)^(1/5) ≈ 1.09812

r ≈ 0.09812 or 9.81% -

Solution:

A = 12000 × (1 + 0.045/12)^(12×8) ≈ 12000 × (1.00375)^96 ≈ 12000 × 1.432364 ≈ $17,188.37

CI = 17188.37 - 12000 ≈ $5,188.37

Combined Exercises: Examples and Solutions

Many mathematical problems require the use of compound interest in conjunction with other operations. Below are examples that incorporate these concepts alongside logical reasoning and application to real-world scenarios.

Example 1: Investment Growth with Regular Contributions

Problem: Emma invests $5,000 in a mutual fund that offers an annual compound interest rate of 6%, compounded annually. She plans to contribute an additional $500 at the end of each year for 5 years. Calculate the total amount in her investment account after 5 years.

Solution:

Future Value of Initial Investment:

A1 = 5000 × (1 + 0.06)^5 ≈ 5000 × 1.338225 ≈ $6,691.13

Future Value of Annual Contributions (Ordinary Annuity):

A2 = 500 × [((1 + 0.06)^5 - 1) / 0.06] ≈ 500 × [1.338225 - 1) / 0.06] ≈ 500 × 5.63708 ≈ $2,818.54

Total Amount = A1 + A2 ≈ 6691.13 + 2818.54 ≈ $9,509.67

Therefore, the total amount in Emma's investment account after 5 years is approximately $9,509.67.

Example 2: Mortgage Calculation with Additional Payments

Problem: Noah takes out a mortgage of $200,000 at an annual compound interest rate of 4%, compounded monthly. He plans to repay the mortgage in 30 years but decides to make an additional payment of $100 every month. Calculate the total amount he will pay over the life of the mortgage.

Solution:

Future Value of Mortgage:

A = 200000 × (1 + 0.04/12)^(12×30) ≈ 200000 × (1.0033333)^360 ≈ 200000 × 3.243397 ≈ $648,679.40

Future Value of Additional Payments:

A2 = 100 × [((1 + 0.04/12)^(12×30) - 1) / (0.04/12)] ≈ 100 × [3.243397 - 1) / 0.0033333] ≈ 100 × [2.243397 / 0.0033333] ≈ 100 × 673.019 ≈ $67,301.90

Total Amount = A + A2 ≈ 648,679.40 + 67,301.90 ≈ $715,981.30

Therefore, Noah will pay a total of approximately $715,981.30 over the life of the mortgage, including the additional payments.

Example 3: Education Savings with Variable Contributions

Problem: Ava wants to save $15,000 for her college education. She invests $10,000 now in an account that offers an annual compound interest rate of 5%, compounded annually. After 3 years, she invests an additional $2,500 at the same interest rate for another 2 years. Calculate the total amount in her account after 5 years.

Solution:

First Investment:

A1 = 10000 × (1 + 0.05)^3 ≈ 10000 × 1.157625 ≈ $11,576.25

Second Investment:

A2 = 2500 × (1 + 0.05)^2 ≈ 2500 × 1.1025 ≈ $2,756.25

Total Amount = A1 + A2 ≈ 11576.25 + 2756.25 ≈ $14,332.50

Therefore, the total amount in Ava's account after 5 years is approximately $14,332.50.

Example 4: Retirement Fund Growth with Regular Contributions

Problem: Liam invests $15,000 in a retirement fund that earns an annual compound interest rate of 6%, compounded annually. He plans to contribute an additional $500 at the end of each year for 20 years. Calculate the total amount in his retirement fund after 20 years.

Solution:

Future Value of Initial Investment:

A1 = 15000 × (1 + 0.06)^20 ≈ 15000 × 3.207135 ≈ $48,107.02

Future Value of Annual Contributions (Ordinary Annuity):

A2 = 500 × [((1 + 0.06)^20 - 1) / 0.06] ≈ 500 × [3.207135 - 1) / 0.06] ≈ 500 × 36.78558 ≈ $18,392.79

Total Amount = A1 + A2 ≈ 48107.02 + 18392.79 ≈ $66,499.81

Therefore, the total amount in Liam's retirement fund after 20 years is approximately $66,499.81.

Example 5: Investment Growth with Variable Rates

Problem: Emma invests $8,000 in an account that offers an annual compound interest rate of 4% for the first 3 years and 5% for the next 2 years, compounded annually. Calculate the total amount in her account after 5 years.

Solution:

First 3 Years at 4%:

A1 = 8000 × (1 + 0.04)^3 ≈ 8000 × 1.124864 ≈ $8,998.91

Next 2 Years at 5%:

A2 = 8998.91 × (1 + 0.05)^2 ≈ 8998.91 × 1.1025 ≈ $9,912.86

Total Amount = A2 ≈ $9,912.86

Therefore, the total amount in Emma's account after 5 years is approximately $9,912.86.

Summary

Understanding and working with compound interest are essential mathematical skills that enable precise financial calculations in various contexts, such as investments, savings, loans, and mortgages. By grasping the fundamental concepts, mastering the compound interest formula, and practicing consistently, you can confidently handle compound interest-related problems.

Remember to:

- Understand the relationship between principal, rate, time, compounding frequency, and compound interest.

- Use the compound interest formula correctly: A = P × (1 + r/n)^(n×t).

- Convert interest rates from percentages to decimals to simplify calculations.

- Identify the compounding frequency to apply the correct value of n.

- Use logarithms to solve for variables like time or rate when necessary.

- Practice converting between percentages, decimals, and fractions to build fluency.

- Break down complex problems into smaller, manageable steps for easier solving.

- Utilize visual aids like charts and graphs to enhance understanding of compound interest growth.

- Double-check your work to ensure accuracy and catch any mistakes.

- Apply compound interest concepts to real-life scenarios to reinforce learning and make the concepts more relatable.

- Practice regularly with a variety of problems to build confidence and proficiency.

- Teach others to reinforce your understanding and identify any areas needing improvement.

With dedication and consistent practice, compound interest will become a fundamental skill in your mathematical toolkit, enhancing your analytical and problem-solving abilities.

Additional Resources

Enhance your learning by exploring the following resources: