🔑 What Is an Auto Loan Calculator?

An Auto Loan Calculator is a financial tool that allows you to calculate your monthly car loan payments based on the loan amount, interest rate, and loan term. It gives you a clear picture of how much you’ll pay each month and the total cost of your car loan over time.

Instead of guessing or manually crunching numbers, the calculator does the heavy lifting—saving you time, effort, and potential mistakes.

💡 Why Use an Auto Loan Calculator?

Plan Your Budget – Know exactly how much your monthly car payment will be and ensure it fits within your financial plan.

Compare Loan Options – Test different loan terms (e.g., 36 months vs. 60 months) and interest rates to find the most affordable option.

Understand Total Costs – See the overall interest you’ll pay across the life of the loan.

Make Smarter Decisions – Use data-driven insights to negotiate better deals with lenders or dealerships.

Save Money – By testing different down payments or loan terms, you can avoid overpaying on interest.

📊 Importance of an Auto Loan Calculator

Buying a car is often the second-largest purchase after a home. With loans running into thousands of dollars, even a small change in the interest rate or loan term can make a huge difference.

The calculator empowers you to:

✅ Avoid surprises with hidden costs

✅ Stay within budget

✅ Make long-term financial decisions confidently

In short, it transforms complex calculations into easy, user-friendly insights.

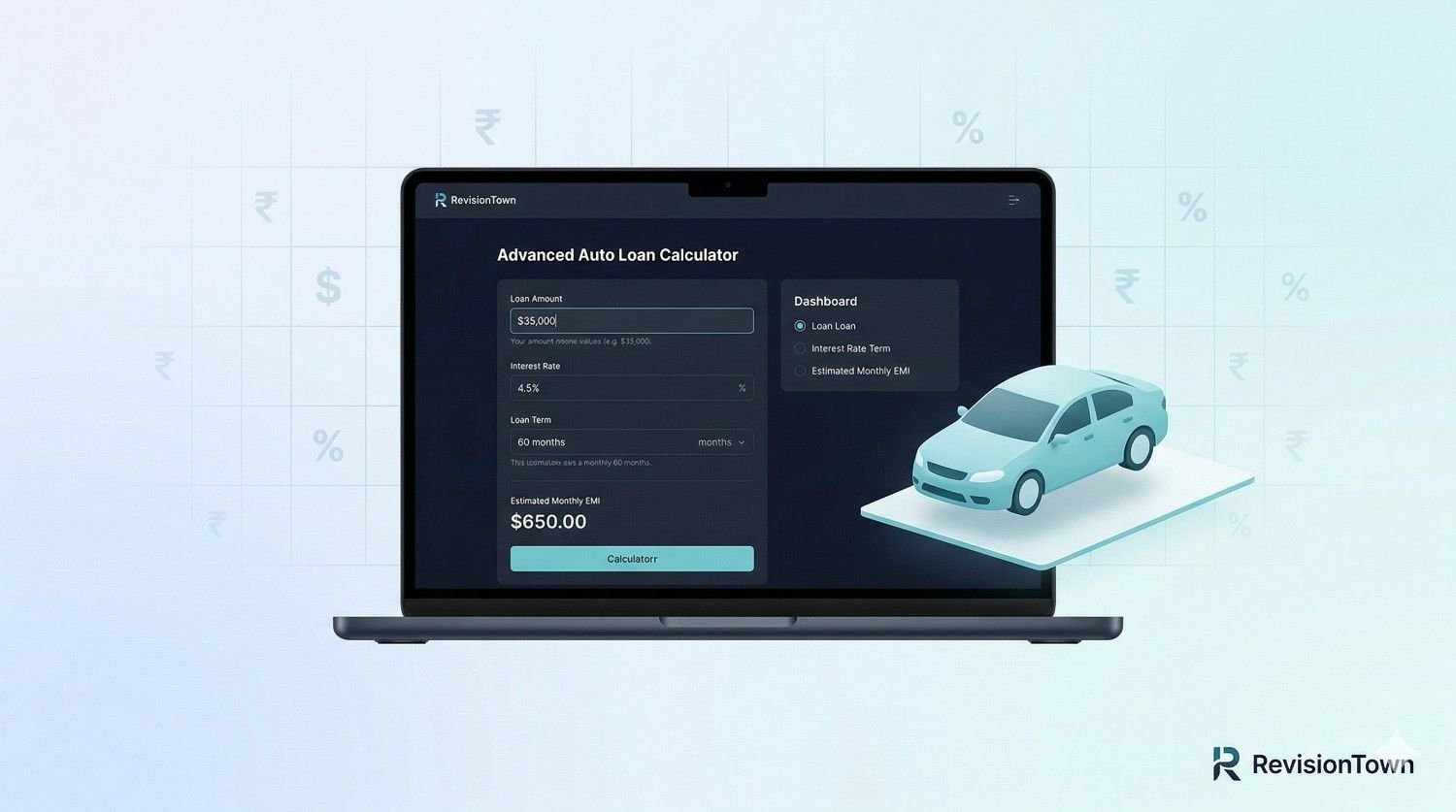

⚙️ How to Use the Auto Loan Calculator

Enter Auto Price – Type in the price of the car you’re planning to buy.

Input Interest Rate – Provide the annual interest rate offered by the lender.

Set Loan Term – Select how many years you want to repay the loan (e.g., 3, 5, or 7 years).

Click Calculate – Instantly get your monthly payment and total loan cost.

❓ Frequently Asked Questions (FAQs)

1. How accurate is the Auto Loan Calculator?

The calculator provides a close estimate. Actual loan payments may vary depending on lender fees, insurance, or additional charges.

2. Can I include a down payment in the calculation?

Yes. Most calculators allow you to input a down payment, which reduces the loan amount and lowers your monthly payments.

3. What’s the best loan term for a car loan?

Shorter terms (e.g., 36 months) have higher monthly payments but lower overall interest. Longer terms (e.g., 72 months) reduce monthly payments but increase total interest costs.

4. Does the calculator include taxes and insurance?

No. It only estimates your loan payment. Taxes, insurance, and registration fees vary by location and must be added separately.

5. Why should I compare interest rates using the calculator?

Because even a 1% difference in interest can save you hundreds or thousands of dollars over the loan period.

🏁 Final Thoughts

The Auto Loan Calculator is your go-to tool for making smarter, stress-free car buying decisions. By understanding your monthly obligations, comparing loan terms, and estimating the total cost, you gain the power to negotiate confidently and avoid financial pitfalls.

💡 Pro Tip: Use the calculator before applying for financing so you know exactly what loan terms you should accept—or reject.